2024-07-24 00:35:02

Shares of CrowdStrike (CRWD 3.43%) sank after the cybersecurity company experienced a major outage that caused disruptions to businesses around the globe. Nonetheless, the stock is still up more than 70% over the past year.

Let’s take a look at the recent outage, the impact it could have on the company moving forward, and whether the dip is a buying opportunity.

Outage impacts customers around the world

The CrowdStrike-related outage stemmed from a bug in a software update the company pushed out. The crash impacted millions of Microsoft Windows devices worldwide, causing Windows-based computers and tablets to crash. The outage impacted numerous industries from governments, to banks, to airlines, which had to cancel flights. Apple and Linux-run devices were not impacted.

The company undid the software update and gave clients a manual workaround to fix affected devices. As such, the company said it may take some time for some systems to be restored.

Microsoft said that about 8.5 million devices were impacted by the outage. While that makes up only about 1% of Windows-based devices, the outage caused widespread disruptions across the globe.

At the very least, this is a bit of a black eye for the company and showed how one mistake can disrupt so much. And while the company likely won’t be financially liable for the outage, it could give some important customers who were overly impacted some price concessions.

Some analysts, such as Wedbush’s Dan Ives, argued the biggest risk to CrowdStrike is that this incident could tarnish its brand and that it opens the door for other cybersecurity companies to take away its business. However, cybersecurity outages are not unique to CrowdStrike and minor ones can be quite common occurrences.

CrowdStrike is still largely considered to be the gold standard for endpoint security, and this outage likely doesn’t change that perception. The disruption caused by the outage also shows just how much CrowdStrike has become ingrained in the IT fabric of industries around the globe and how important the company is.

Cybersecurity companies have recently been pushing customers to consolidate on one platform, arguing that they get better protection from a unified system that works together compared to stringing disparate endpoint solutions together. It will be interesting to see if customers continue down this path or want to keep multiple vendors.

That said, I don’t think that this outage by itself will have any long-term implications for CrowdStrike or its stock, as organizations will ultimately continue to gravitate toward best-of-breed cybersecurity solutions.

Image source: Getty Images.

Is it time to buy the dip?

While I don’t think the outage will have any lasting impact on CrowdStrike’s long-term prospects, whether now is a good time to buy the dip in stock price is a whole different question. The one knock on CrowdStrike has been its hefty valuation, and the recent dip in the stock price did not suddenly put it into bargain-bin territory.

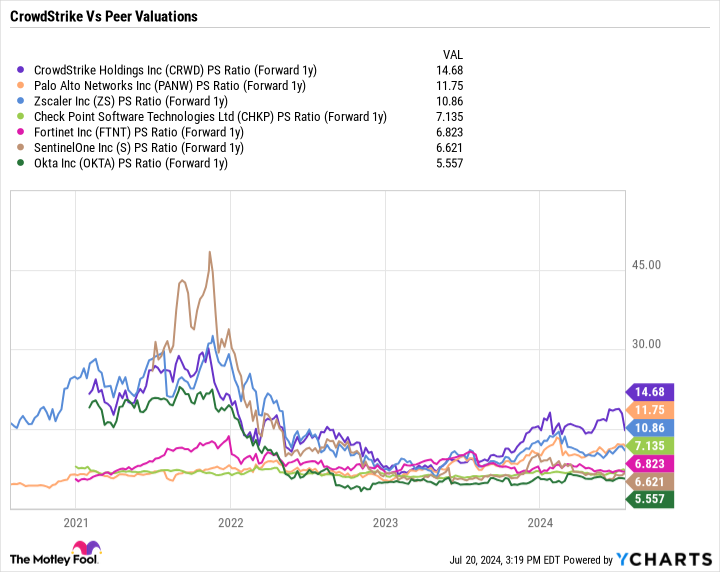

The stock now trades at a forward price-to-sales (P/S) ratio based on fiscal 2026 (ending January) estimates of about 14.7 times. That is still the highest valuation among its cybersecurity peers. The company is growing strongly, putting up 33% revenue growth in the first quarter, but other peers have also shown strong revenue growth as well. For example, SentinelOne grew its revenue 40% in Q1, while Zscaler saw its revenue rise 32% for its most recent quarter.

CRWD PS Ratio (Forward 1y) data by YCharts

Given its premium valuation, I wouldn’t jump into CrowdStrike’s stock just yet. However, if the outage causes the stock to continue to trend lower, closer to the valuations of other cybersecurity stocks, I would become more interested in owning the stock.

I continue to view CrowdStrike as best of breed in the cybersecurity space, but valuation does still matter.

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Check Point Software Technologies, CrowdStrike, Fortinet, Microsoft, Okta, Palo Alto Networks, and Zscaler. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.