2024-08-06 00:10:01

Matteo Colombo

Investment thesis

My previous bullish thesis about the SPDR® S&P 500 ETF Trust (SPY, SP500) kept up well before today’s morning, as there is a massive panic around the U.S. stock market after the Japanese stock market’s crash.

I think that SPY’s 4% dip that I see currently during pre-market hours, is a big overreaction. The last week’s uptick in the unemployment rate does not look like something unexpected and disastrous, in my opinion.

Moreover, it appears that all other notable recent developments are mostly quite bullish for the broader U.S. stock market. The Q2 earnings season demonstrates positive trends in the largest companies’ earnings. Strong corporate performance of the U.S. businesses underpins the strength of the world’s largest economy. Overall, I remain very bullish about the U.S. stock market, and the robust Q2 earnings season so far makes me reiterate a “Strong Buy” rating for SPY.

Recent developments

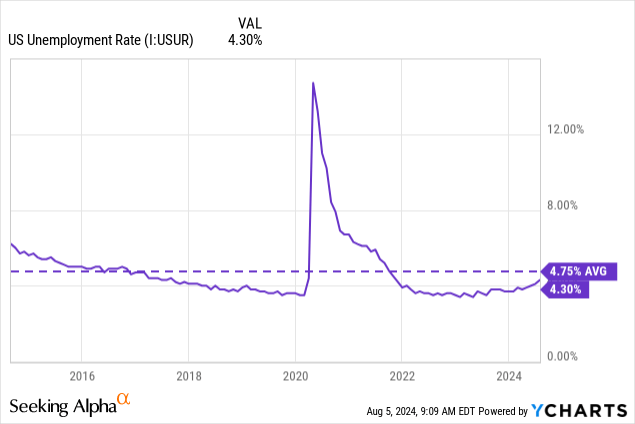

Today’s Japanese stock market’s crash is explained by the uptick in the U.S. unemployment rate released late last week. The unemployment rate grew to 4.3% in July, which was absorbed by the market with panic. I think that there are two big reasons not to panic.

First, the current 4.3% unemployment level is still notably below compared to the last decade’s average of 4.75%. Moreover, current unemployment level is close to pre-pandemic levels. As long as the unemployment rate aligns with long-term historical averages and pre-pandemic levels, I think that there are no reasons to panic.

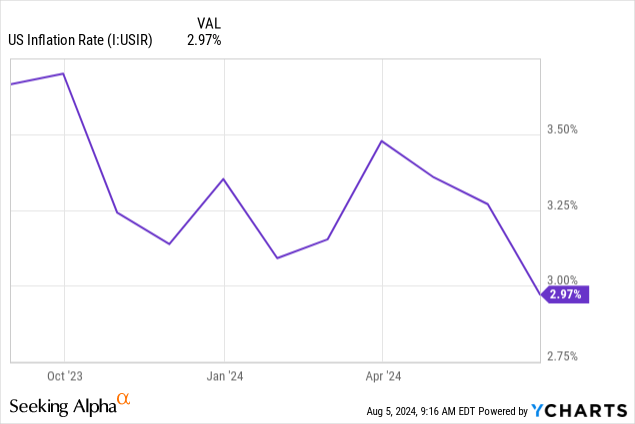

The second reason to remain positive is that, despite an uptick in unemployment, we are now very close to the Fed’s target levels announced in the early months of its monetary policy tightening cycle. In September 2022, it was announced that the Fed’s officials projected a 4.4% unemployment rate as a result of the monetary policy tightening. Since inflation is heading down and the unemployment rate moving closer to the Fed’s targets, I think that the Fed is now ready to start cutting interest rates.

Moreover, in June 2024 the World Bank upgraded its outlook for the global economy, and the resilience of the U.S. economy was the primary reason for this optimism. This is another positive sign, in my opinion.

We also should not ignore that the largest U.S. companies demonstrated strong flexibility and adaptability to the harsh monetary environment. We have an ongoing Q2 2024 earnings season and almost all financial and technological giants already shared their quarterly reports. The earnings season commenced with the top banks reporting their Q2 results, which were solid, and the Q3 outlook from Wall Street analysts appear to be predominantly positive as well. The consistently strong performance of the top-3 U.S. banks means that the overall corporate America is likely to be in good condition too.

Compiled by the author

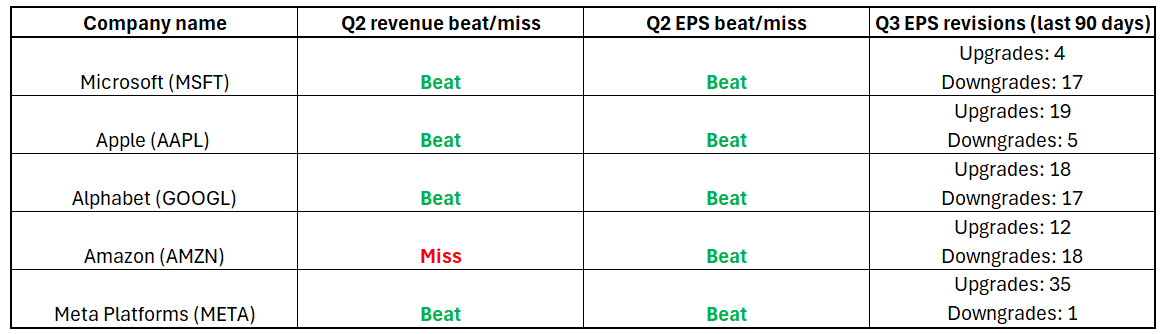

Apart from the largest banks, 6 out of the top-10 holdings [Google is presented with two different stock classes] in the SPY portfolio also reported their Q2 earnings, and I see many positive moments here as well. As shown in the below table, the largest SPY holdings delivered positive revenue and EPS surprises against consensus estimates, except for Amazon’s (AMZN) slightly missing on revenue consensus estimates.

From the below table, we can also see that Wall Street analysts’ expectations around Q3 earnings are mostly favorable because there were much more EPS upgrades than downgrades over the last three months. Thus, the largest SPY holdings delivered strong Q2 earnings and the Q3 outlook is predominantly positive. Other hyper-scalers like Nvidia (NVDA), Broadcom (AVGO), and Eli Lilly (LLY) are still to report their calendar Q2 2024 earnings.

Compiled by the author

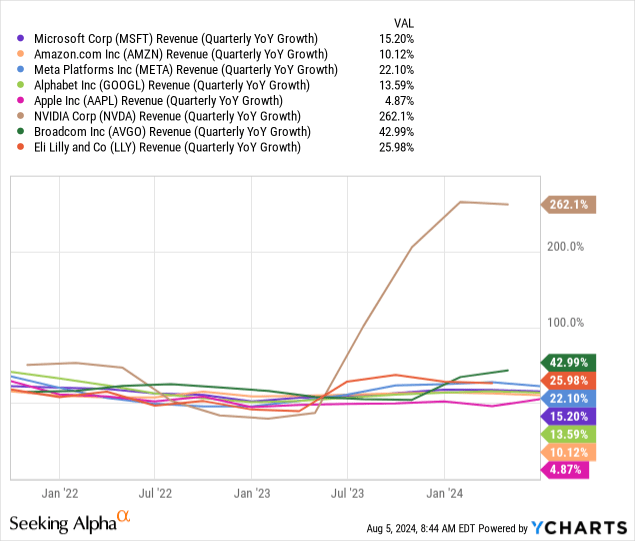

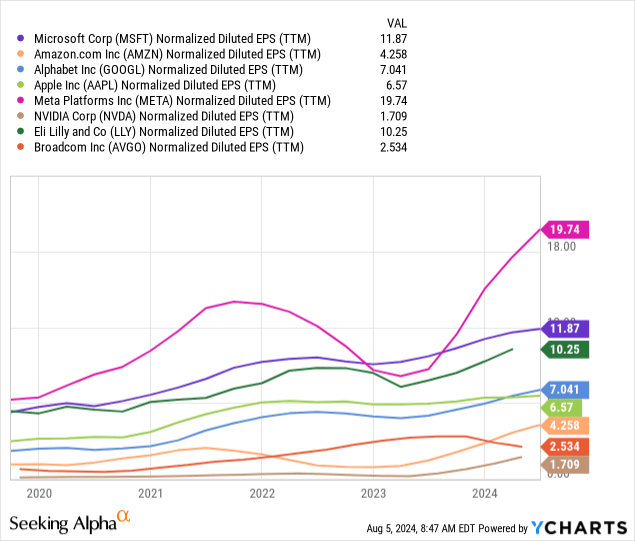

What is also crucial is that the revenues of five out of six of these largest companies are looking up. Apple’s (AAPL) revenue is an exception, but its struggles are caused by company-specific problems, in my opinion. As shown below, other largest tech players demonstrate impressive revenue growth trajectories.

The health of corporate revenues is crucial because it appears to me that America’s largest corporations have been quite successful in addressing the tight monetary environment with stringent cost discipline. Profits of the largest SPY holdings appear to be at record highs, and all of them demonstrate positive TTM dynamic. It is also remarkable that EPS of giants are higher than pandemic levels when businesses navigated very favorable monetary environment. Record layoffs of 2022-2023 helped giants to improve profitability, and most of them continue seeking for more efficiency as they continue cutting some positions.

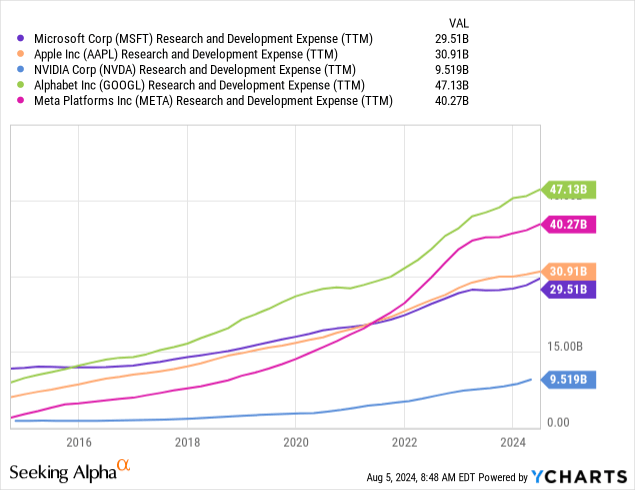

In the below chart, readers can find one more reason to remain bullish. The largest U.S. Tech companies are currently investing in R&D much more than they ever did before. Tech giants’ R&D budgets are ramping up as the Artificial Intelligence [AI] race continues. This likely means that top management of these companies are quite confident in future growth and the potential to create more value to shareholders.

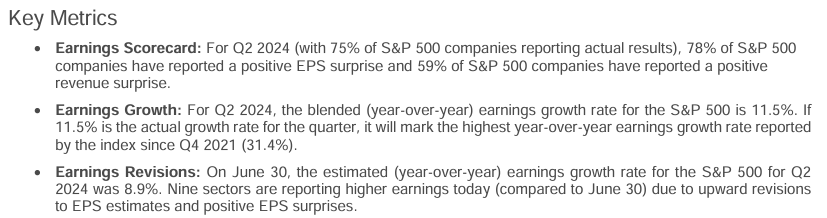

The S&P 500 consists of hundreds of other companies beyond the largest banks and tech corporations. Therefore, I have to elaborate more on how the Q2 earnings season is going so far. According to the latest “Earnings Insight” update from FactSet, 75% of S&P500 companies reported their Q2 earnings and the dynamic is quite positive.

FactSet

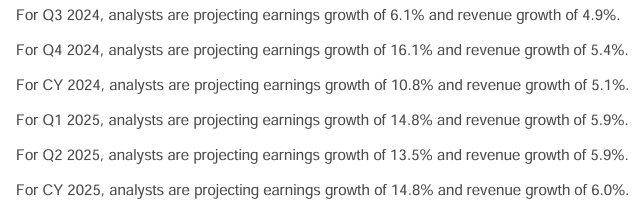

Apart from strong Q2 performance across most of the S&P 500 companies, I also must highlight that the outlook for the remainder of 2024 is also quite positive and FactSet expects revenue and earnings growth to accelerate in Q3-Q4. The outlook for 2025 is also positive, with the projected average 6.0% revenue growth and 14.8% earnings growth.

FactSet

To summarize the fundamental part, most of the developments suggest that the U.S. stock market has rock-solid fundamentals. Corporate profits continue expanding despite interest rates remaining at multi-decade highs, which backs the overall health of the U.S. economy. In turn, the strong U.S. economy is the cornerstone of the global economic prosperity, and this positive stance gives me high conviction in the fundamental strength of the U.S. stock market.

Now, let us move to specific names and tickers. I, personally, prefer to collect SPY in my portfolio because it is the oldest and most liquid ETF which is focused on S&P 500. It is my personal preference, despite SPY having the highest among peers’ expense ratios. Investors should be aware that there are two more prominent S&P 500 ETFs, the iShares Core S&P 500 (IVV) and Vanguard’s S&P 500 ETF (VOO). These ETFs provide even slightly better long-term performance compared to SPY due to lower expense ratios. Which one to select is up to every investor’s personal priority, and liquidity matters to me.

Compiled by the author

Since all three ETFs track the same strategy, I think that my fundamental analysis of recent developments applies to all three. I consider all three of them to be a compelling investment opportunity, and SPY is the one I personally buy.

Risks update

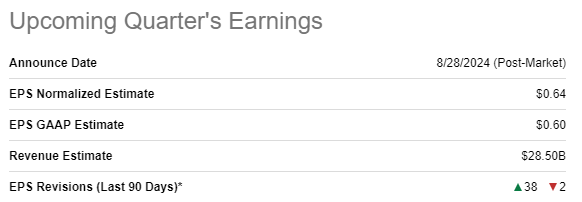

The most important stock on Earth currently, NVDA, has not reported its latest quarterly results yet. The company releases its calendar Q2 2024 earnings on August 28 and expectations are running extremely hot with 38 EPS upgrades from Wall Street analysts over the last 90 days. Generally, I consider upward EPS revisions to be a bullish sign. However, the quantity of EPS upgrades for NVDA appears to be extremely high. Investors should keep in mind that the moon has two sides, and expectations might go way higher than NVDA’s real potential to deliver positive surprise as a result of Q2. NVDA represents 5.9% of SPY’s portfolio, meaning that the exposure is limited and the direct effect of a potential sell-off in NVDA might not be significant. However, a sell-off in NVDA might lead to panic in the whole Technology sector, which currently represents 31.6% of the broader U.S. market.

Seeking Alpha

The political uncertainty in the U.S. is extremely high and is expected to expand as the 2024 Presidential elections are approaching. I doubt that the winner of the election race will significantly affect the economic growth potential of the U.S. or will be able to affect the Fed’s decisions regarding monetary policy. However, the health of the U.S. companies’ corporate profits notably depends on geopolitical relationships with China, the world’s second economy and one of the most important U.S. trade partners. Therefore, some hot headlines regarding worsening relationships between the U.S. and China might deteriorate investors’ sentiment.

Bottom line

To conclude, I believe that SPY is a “Strong Buy” at the moment. The U.S. economy demonstrates rock-solid resilience, which is a big catalyst for the global economy’s health as well. This broader economy’s strength is backed by the health of the corporate America, as the country’s largest corporations continue demonstrating impressive trends in their earnings.